Seller’s Closing Costs Explained: What Home Sellers Really Pay at Closing in the U.S.

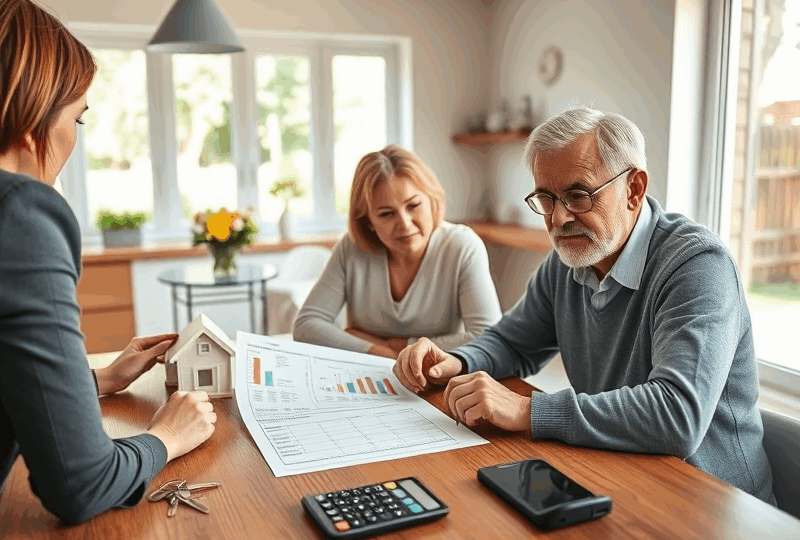

Selling a home in the United States can be an exciting yet financially complex process. While many sellers focus on the sale price, it’s equally important to understand the closing costs involved. These are the fees and expenses that sellers are responsible for paying at the end of a real estate transaction. In this guide, we’ll break down the typical seller’s closing costs, how much you can expect to pay, and what factors influence these expenses.

What Are Seller’s Closing Costs?

Seller’s closing costs are the fees and charges that a home seller must pay when transferring ownership of their property to a buyer. These costs are typically deducted from the proceeds of the home sale and can vary based on location, property value, and terms of the sale.

Common seller closing costs include:

– Real estate agent commissions

– Title insurance

– Transfer taxes

– Escrow fees

– Attorney fees (in some states)

– Repairs or credits to the buyer

– Outstanding liens or mortgage payoff

Real Estate Agent Commissions

One of the largest closing costs for sellers is the real estate agent commission. In most U.S. markets, the seller pays the commission for both their agent and the buyer’s agent. This typically totals 5% to 6% of the home’s sale price.

For example, if you sell your home for $400,000, you might pay $24,000 in commissions. While this is negotiable, it’s standard practice in many areas.

Title Insurance and Title Fees

Title insurance protects the buyer and lender from potential issues with the property’s title, such as liens or ownership disputes. In many states, the seller pays for the buyer’s title insurance policy. This cost can range from a few hundred to a few thousand dollars, depending on the home’s value and location.

Additionally, there may be title search fees and other administrative charges from the title company.

Transfer Taxes and Recording Fees

Transfer taxes are levied by state or local governments when property changes hands. These taxes vary widely by state and even by county. For example, in New York City, transfer taxes can be over 1.4% of the sale price, while some states like Texas do not charge a transfer tax at all.

Recording fees are smaller charges paid to the local government to record the change in property ownership.

Escrow and Attorney Fees

Escrow fees are paid to the escrow company that handles the funds and documents during the closing process. These fees are usually split between the buyer and seller, but the exact arrangement can vary.

In some states, such as New York and Illinois, it’s customary for both parties to have legal representation. Attorney fees for sellers can range from $500 to $1,500 or more, depending on the complexity of the transaction.

Repairs and Buyer Credits

During the home inspection, buyers may request repairs or credits for issues found. Sellers can either fix the problems before closing or offer a credit to the buyer. These costs are negotiable but can significantly impact your net proceeds.

Mortgage Payoff and Prepayment Penalties

If you still owe money on your mortgage, the remaining balance must be paid off at closing. Be sure to check with your lender about any prepayment penalties or additional fees for early payoff.

Home Warranty (Optional)

Some sellers offer a home warranty to make their property more attractive to buyers. This typically costs between $300 and $600 and covers repairs for major systems and appliances for the first year after purchase.

How Much Do Sellers Typically Pay?

According to data from Zillow and the National Association of Realtors, seller closing costs in the U.S. typically range from 6% to 10% of the home’s sale price. This includes agent commissions and all other fees.

For example:

– On a $300,000 home, expect to pay between $18,000 and $30,000 in closing costs.

– On a $500,000 home, costs could range from $30,000 to $50,000.

Can You Reduce Seller Closing Costs?

Yes, there are several ways to reduce your closing costs:

– Negotiate lower agent commissions

– Shop around for title and escrow services

– Avoid unnecessary seller concessions

– Sell your home “as-is” to limit repair costs

Working with an experienced real estate agent can also help you navigate these costs and identify areas where you can save.

State-by-State Variations

Closing costs can vary significantly by state due to differences in taxes, regulations, and customary practices. For example:

– In California, sellers often pay for the buyer’s title insurance and escrow fees.

– In Florida, sellers typically pay for the deed transfer tax.

– In Texas, the buyer usually pays for title insurance.

It’s important to consult with a local real estate professional or attorney to understand the specific costs in your area.

Final Thoughts

Understanding seller closing costs is essential for accurately estimating your net proceeds from a home sale. While these costs can be substantial, being informed and prepared can help you make smarter financial decisions and avoid surprises at the closing table.

Disclaimer

This article is for informational purposes only and does not constitute legal, financial, or real estate advice. Always consult with a licensed real estate professional, attorney, or financial advisor regarding your specific situation. Real estate laws and practices vary by state and may change over time. We do not guarantee the accuracy or completeness of the information provided.

Sources

– National Association of Realtors (www.nar.realtor)

– Zillow Research (www.zillow.com/research)

– U.S. Department of Housing and Urban Development (www.hud.gov)

답글 남기기