Mortgage Process Guide: How to Secure a Home Loan Smoothly in the U.S.

Buying a home is one of the most significant financial decisions you’ll make in your lifetime. Whether you’re a first-time homebuyer or looking to refinance, understanding the mortgage process in the United States can help you navigate it with confidence and avoid unnecessary stress. In this comprehensive guide, I’ll walk you through each step of the mortgage process, offering expert insights and practical tips to make your home loan journey as smooth as possible.

Understanding What a Mortgage Is

A mortgage is a loan used to purchase a home or other real estate. The property itself serves as collateral for the loan. In the U.S., mortgages are typically repaid over 15 to 30 years through monthly payments that include principal and interest, and often property taxes and homeowners insurance.

There are several types of mortgages available, including:

– Conventional Loans

– FHA Loans (Federal Housing Administration)

– VA Loans (for veterans and active military)

– USDA Loans (for rural properties)

Each type has its own eligibility requirements, benefits, and drawbacks. It’s important to understand which loan type best suits your financial situation and long-term goals.

Step 1: Check Your Credit Score

Your credit score plays a crucial role in determining your mortgage eligibility and interest rate. Most lenders require a minimum credit score of 620 for conventional loans, although government-backed loans like FHA may accept lower scores.

You can check your credit score for free through AnnualCreditReport.com, the only federally authorized source for free credit reports from the three major bureaus: Equifax, Experian, and TransUnion.

Tips to improve your credit score:

– Pay bills on time

– Reduce credit card balances

– Avoid opening new credit accounts before applying for a mortgage

Step 2: Determine How Much You Can Afford

Before shopping for a home, it’s essential to determine your budget. Lenders use a metric called the debt-to-income (DTI) ratio to assess your ability to repay the loan. Most lenders prefer a DTI ratio below 43%.

Use online mortgage calculators to estimate your monthly payments based on different loan amounts, interest rates, and down payments. Don’t forget to factor in property taxes, homeowners insurance, and potential HOA fees.

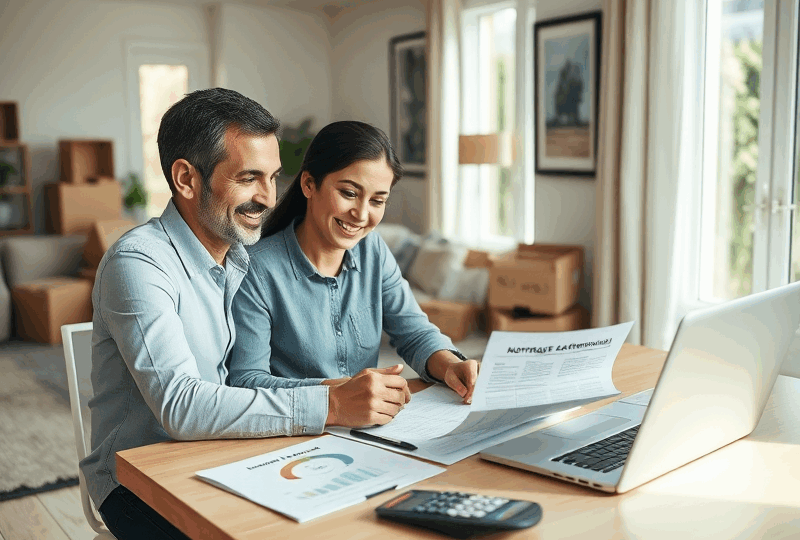

Step 3: Get Pre-Approved for a Mortgage

Getting pre-approved shows sellers that you’re a serious buyer and gives you a clear idea of your borrowing capacity. During pre-approval, a lender will evaluate your credit, income, assets, and debts.

Documents typically required for pre-approval:

– Recent pay stubs

– W-2 forms or tax returns (last 2 years)

– Bank statements

– Proof of assets

– Employment verification

Pre-approval letters are usually valid for 60 to 90 days.

Step 4: Shop for the Right Mortgage Lender

Not all lenders offer the same rates or terms. It’s wise to shop around and compare quotes from multiple lenders, including banks, credit unions, and online mortgage companies.

Key factors to compare:

– Interest rates (fixed vs. adjustable)

– Loan terms (15-year vs. 30-year)

– Closing costs

– Lender fees

According to the Consumer Financial Protection Bureau (CFPB), comparing offers can save you thousands over the life of your loan.

Step 5: Find Your Dream Home and Make an Offer

Once pre-approved, you can start house hunting with confidence. Work with a licensed real estate agent who understands your needs and local market conditions.

When you find the right home, your agent will help you submit a competitive offer. If accepted, you’ll enter into a purchase agreement and begin the mortgage application process.

Step 6: Apply for the Mortgage

Even if you’ve been pre-approved, you’ll still need to formally apply for the mortgage. This involves submitting updated financial documents and authorizing a credit check.

Your lender will provide a Loan Estimate within three business days, outlining the terms, interest rate, monthly payment, and closing costs.

Step 7: Home Appraisal and Inspection

Lenders require a home appraisal to ensure the property is worth the loan amount. This protects both you and the lender from overpaying.

A home inspection, while not mandatory, is highly recommended. It can uncover hidden issues such as structural damage, plumbing problems, or outdated electrical systems.

Step 8: Underwriting Process

During underwriting, the lender reviews all your financial information and the property details to assess risk. They may request additional documentation or clarification.

This step can take anywhere from a few days to several weeks, depending on the complexity of your application.

Step 9: Closing the Loan

Once your loan is approved, you’ll receive a Closing Disclosure at least three business days before your closing date. This document outlines your final loan terms and closing costs.

At closing, you’ll sign all necessary paperwork, pay any remaining fees, and receive the keys to your new home. Congratulations!

Common Mistakes to Avoid

– Making large purchases before closing

– Changing jobs during the mortgage process

– Not locking in your interest rate

– Ignoring closing costs

Avoiding these mistakes can help ensure a smooth and successful mortgage experience.

Final Thoughts

Securing a mortgage doesn’t have to be overwhelming. By understanding each step of the process and preparing in advance, you can confidently move forward on your path to homeownership. Always consult with licensed mortgage professionals and use trusted resources like the CFPB (consumerfinance.gov) and HUD (hud.gov) for up-to-date information.

Disclaimer

This article is for informational purposes only and does not constitute financial, legal, or real estate advice. Always consult with a licensed mortgage lender, financial advisor, or attorney before making any financial decisions. The author and publisher are not responsible for any outcomes resulting from the use of this information.

답글 남기기